Bitcoin vs. Traditional Banking: What’s the Future? Yo, this ain’t your grandpa’s bankin’. We’re talkin’ digital gold rush vs. the established financial system.

Bitcoin’s all about decentralization and blockchain tech, while traditional banks are, well, traditional. This battle of the titans is about more than just money; it’s about control, speed, security, and who gets to call the shots in the future of finance. Get ready to peep the lowdown on both sides and see which one’s gonna reign supreme.

This deep dive into Bitcoin and traditional banking will explore the core differences, from security measures and transaction speeds to accessibility and investment opportunities. We’ll also examine the potential future of both systems, considering emerging technologies and societal shifts. It’s a wild ride, so buckle up!

Introduction to Bitcoin and Traditional Banking: Bitcoin Vs. Traditional Banking: What’s The Future?

The digital revolution has unleashed a seismic shift in financial landscapes, pitting the revolutionary cryptography of Bitcoin against the age-old, established structures of traditional banking. This clash of titans reverberates through the global economy, promising both unprecedented opportunity and potentially devastating disruption. The future of finance hangs in the balance, a battleground where innovation and tradition grapple for dominance.Bitcoin, a decentralized digital currency, operates outside the traditional financial system, challenging the very foundations of monetary authority.

Traditional banking, on the other hand, represents a centuries-old network of institutions that underpin the global economy, facilitating transactions and managing assets for billions. Their contrasting approaches to finance represent a fundamental divergence in how value is created, exchanged, and secured.

Defining Bitcoin

Bitcoin is a decentralized digital currency, operating on a peer-to-peer network secured by cryptography. Its unique characteristic is its immutability and transparency, allowing for transactions to occur without intermediaries like banks. Bitcoin’s underlying technology, the blockchain, records all transactions in a public ledger, creating a tamper-proof history of ownership. This cryptographic nature, coupled with limited supply, has made Bitcoin a subject of intense speculation and scrutiny.

Deconstructing Traditional Banking

Traditional banking systems are complex networks of institutions that facilitate financial transactions, manage assets, and provide credit to individuals and businesses. Centralized control, established regulatory frameworks, and a reliance on physical infrastructure define their fundamental structure. These systems act as intermediaries, holding and transferring funds between parties, playing a vital role in the global economy.

Contrasting Technologies and Structures

Bitcoin’s decentralized nature contrasts sharply with the centralized structure of traditional banking. Bitcoin’s technology, the blockchain, is a distributed ledger that allows for transparent and verifiable transactions, eliminating the need for a central authority. Traditional banking, conversely, relies on a network of institutions overseen by regulatory bodies, facilitating transactions through a complex web of financial instruments and procedures.

Historical Context

Traditional banking emerged gradually over centuries, adapting to evolving economic needs. Bitcoin, a relatively recent innovation, emerged from the digital revolution, challenging the existing paradigm with its decentralized approach. The contrasting trajectories of these two systems highlight the rapid pace of technological advancement and its impact on financial systems.

Core Differences

| Characteristic | Bitcoin | Traditional Banking |

|---|---|---|

| Ownership | Decentralized, held by individuals via digital wallets | Centralized, held by institutions |

| Transaction Speed | Generally faster for peer-to-peer transactions | Variable, depending on the system and complexity of transaction |

| Security | Secure due to cryptography and decentralized nature | Secure with robust systems, but vulnerabilities exist |

This table summarizes the fundamental distinctions between the two systems, highlighting the decentralized nature of Bitcoin and the centralized structure of traditional banking.

Security and Regulation

The digital realm, a battlefield of unprecedented opportunity and peril, presents a stark contrast between the established fortress of traditional banking and the volatile frontier of Bitcoin. This clash of systems manifests most dramatically in their security postures and regulatory landscapes. One is built on centuries of trust and painstakingly crafted safeguards, while the other operates on a decentralized ledger, inviting unique challenges and opportunities.

Both systems are vulnerable to attack, but their vulnerabilities differ fundamentally.Traditional banking, despite its apparent stability, has been plagued by monumental failures, highlighting the inherent risks of centralized systems. Bitcoin, conversely, boasts the allure of decentralization, but this very characteristic also exposes it to novel and unforeseen threats. The regulatory landscape further complicates the comparison, with traditional banking operating under well-established frameworks and Bitcoin navigating a turbulent sea of evolving policies.

Bitcoin Transaction Security

Bitcoin’s security relies on cryptography, employing complex algorithms to secure transactions and verify the authenticity of digital signatures. These cryptographic protocols, while robust, are not invulnerable. The distributed nature of the Bitcoin network, while a strength, also introduces potential points of failure if not meticulously maintained. Furthermore, the inherent volatility of the cryptocurrency market and the potential for malicious actors to exploit vulnerabilities pose significant security challenges.

Bitcoin’s security is fundamentally dependent on the integrity of its network participants and the resilience of the underlying cryptographic algorithms.

Traditional Banking Security

Traditional banking systems employ a multitude of security measures, ranging from physical security protocols to sophisticated encryption techniques and advanced fraud detection systems. Centralized control allows for coordinated responses to threats and enables the deployment of significant resources for security investment. However, these centralized systems are also vulnerable to systemic risks, such as cyberattacks targeting critical infrastructure or failures within the banking network.

These failures can have catastrophic consequences, as demonstrated by past financial crises.

Regulatory Frameworks

Traditional banking operates under a complex network of regulatory frameworks designed to maintain stability, prevent fraud, and protect consumers. These frameworks, while often robust, are subject to constant evolution to address emerging threats and adapt to changing economic landscapes. Bitcoin, in contrast, operates in a largely unregulated space, creating a fertile ground for illicit activities and posing significant challenges for legitimate users.

The lack of a universally accepted regulatory framework for cryptocurrencies leads to inconsistencies and uncertainty across jurisdictions.

Comparison of Resilience to Cyberattacks

Bitcoin’s decentralized architecture makes it theoretically more resilient to targeted attacks on a single point of failure. However, concentrated attacks on the network’s overall integrity can still have devastating effects. Traditional banking systems, while centralized, have developed robust defenses against cyberattacks. However, sophisticated attacks can exploit vulnerabilities in the interconnected network of financial institutions. The recent history of cyberattacks on banks highlights the continuous need for robust defenses and vigilance.

Potential Risks

Both Bitcoin and traditional banking systems face potential risks. Bitcoin’s inherent volatility and susceptibility to price manipulation pose significant risks to investors. The lack of consumer protection in the cryptocurrency market can lead to substantial financial losses. Traditional banking systems, while seemingly stable, can face systemic risks due to economic downturns, regulatory failures, and unforeseen events. Financial crises, like the 2008 global financial crisis, serve as stark reminders of the potential for systemic failures in traditional banking systems.

Regulatory Landscape Comparison

| Jurisdiction | Bitcoin Regulation | Traditional Banking Regulation |

|---|---|---|

| United States | Varied, with ongoing debate and patchwork of state and federal regulations. | Stringent and comprehensive, with regulatory oversight from the Federal Reserve, FDIC, and other bodies. |

| European Union | Evolving regulations, focusing on consumer protection and market integrity. | Well-established regulatory framework with the European Central Bank and national regulators playing a critical role. |

| China | Highly restrictive, with a near-complete ban on cryptocurrency transactions. | Robust regulatory framework, with the People’s Bank of China overseeing the financial system. |

| Japan | More supportive approach, with a framework aimed at fostering innovation while maintaining consumer protection. | Strict regulatory oversight by the Bank of Japan and financial authorities. |

The table above illustrates the varied regulatory approaches to Bitcoin and traditional banking across different jurisdictions. These differences highlight the complexities of regulating emerging technologies in the face of established financial systems. These differing approaches underscore the significant regulatory challenges facing both the cryptocurrency and traditional financial industries.

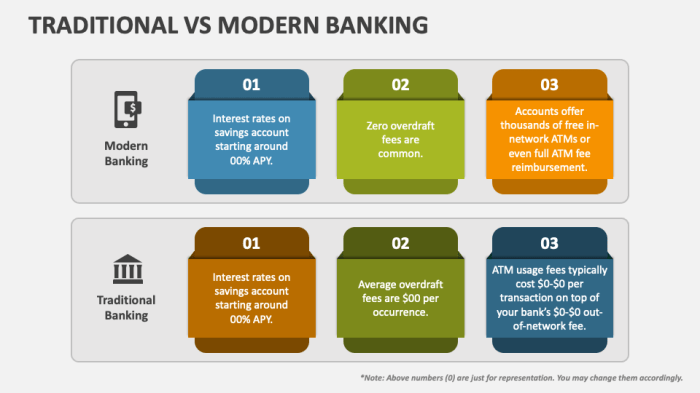

Transaction Speed and Costs

The digital realm of finance is a battleground of speed and efficiency. Bitcoin, the revolutionary cryptocurrency, promises lightning-fast transactions, while traditional banking, a behemoth of established processes, grapples with its own complexities. The disparity in transaction speeds and associated costs between these two systems dictates their respective appeal and future viability. The very nature of these differences is poised to reshape the financial landscape, leaving a trail of winners and losers in its wake.

Bitcoin Transaction Speed

Bitcoin’s transaction speed, while revolutionary in its potential, is not without its limitations. The blockchain, the immutable ledger underpinning Bitcoin, processes transactions in blocks, a process that, while transparent, is inherently finite. Confirmation times, though often quoted as minutes, can vary significantly based on network congestion. High transaction volume can lead to delays, a crucial point when assessing the practicality of Bitcoin for everyday transactions.

Furthermore, transaction fees, though typically lower than traditional banking fees for domestic transfers, can still be significant for large transactions.

Bitcoin Transaction Costs

The cost of a Bitcoin transaction is dynamic, fluctuating based on network demand. Transaction fees, expressed in Bitcoin, are influenced by factors such as the desired confirmation time and the current transaction volume. While seemingly low compared to some traditional banking fees, these costs can accumulate for frequent or high-volume users. The volatility of Bitcoin’s price further complicates the cost analysis, as transaction fees are denominated in Bitcoin, potentially leading to substantial variations in their real-world value.

Traditional Banking Transaction Speed

Traditional banking systems, despite their global reach, often struggle with speed, particularly in international transfers. This is due to the complex, multi-layered nature of the process, involving various institutions and regulatory hurdles. Processing times for international wire transfers can span several days, significantly impacting businesses and individuals requiring rapid international payments. The intricate web of correspondent banking relationships often adds layers of complexity, slowing down the entire process.

Traditional Banking Transaction Costs

The costs associated with traditional banking transactions are often opaque and multi-faceted. International wire transfers, for example, typically involve charges from each bank involved in the transaction, as well as potentially hefty exchange fees. These charges can vary widely based on the specific banks involved and the amount being transferred, and are often not immediately apparent to the user.

Domestic transfers, while faster, are not without their associated fees, which may be calculated per transaction or as a percentage of the amount transferred.

Comparison of Transaction Speeds and Costs

A direct comparison of Bitcoin and traditional banking reveals stark contrasts. Bitcoin’s decentralized nature allows for faster, albeit potentially variable, domestic transactions, often at lower fees. However, international transfers using Bitcoin still face limitations in terms of speed and regulatory acceptance. Traditional banking, despite its global reach, often suffers from delays in international transfers, coupled with higher, more predictable costs.

Factors Influencing Transaction Speed and Costs in Bitcoin

Several factors influence Bitcoin transaction speed and costs. Network congestion is a primary driver, impacting both confirmation times and fees. The level of transaction volume directly impacts the time required for confirmations. Transaction fees are also influenced by the desired confirmation time, with faster confirmations generally commanding higher fees.

Factors Influencing Transaction Speed and Costs in Traditional Banking

The factors influencing traditional banking transaction speed and costs are multifaceted and deeply embedded within the established infrastructure. Correspondent banking relationships, regulatory compliance, and the volume of transactions processed by each bank all play a role. International transfers are often affected by exchange rate fluctuations, which can add to the overall cost.

Procedures for Sending and Receiving Money Using Bitcoin

Sending Bitcoin typically involves generating a Bitcoin address, creating a transaction, and broadcasting it to the network. Confirmation of the transaction is based on the inclusion of the transaction in a block of transactions on the blockchain. Receiving Bitcoin involves having a Bitcoin address that is used as a destination for the transaction.

Procedures for Sending and Receiving Money Using Traditional Banking

Sending money through traditional banking involves creating a wire transfer request, providing recipient details, and adhering to the bank’s specific procedures. Receiving money typically involves having an account at the recipient bank, which will process the transfer once the instructions are received.

Accessibility and Inclusivity

The digital frontier of finance, once a bastion of the privileged few, now faces a seismic shift. Bitcoin, with its decentralized ethos, promises a revolutionary reimagining of financial access, while traditional banking grapples with its legacy infrastructure. This clash of titans, however, is not a simple dichotomy. Each system presents unique strengths and weaknesses when scrutinized through the lens of accessibility and inclusivity.The very nature of Bitcoin’s decentralized architecture, while lauded for its potential, also presents significant hurdles in terms of widespread adoption.

Conversely, the entrenched global network of traditional banking, despite its limitations, holds considerable sway in established financial landscapes. The chasm between these two systems reveals a complex tapestry of opportunities and challenges, where the underserved are poised to be either empowered or further marginalized.

Bitcoin’s Global Reach

Bitcoin’s decentralized nature, while ostensibly liberating, faces the stark reality of uneven global access. Its reliance on internet connectivity and digital literacy presents a formidable barrier in regions with limited infrastructure. While Bitcoin proponents envision a world where anyone with a smartphone can participate in the global financial system, the reality is far more nuanced. Transactions are often subject to high volatility, making it a risky proposition for those with limited financial capital.

Traditional Banking’s Regional Variations

Traditional banking systems, despite their global reach, exhibit significant disparities in accessibility across different regions. Developed nations typically boast robust financial infrastructure, enabling widespread access to banking services. However, in developing economies, access remains a significant challenge, often exacerbated by limited infrastructure, inadequate regulatory frameworks, and high transaction costs. Furthermore, cultural norms and financial literacy levels play a critical role in shaping the accessibility of banking services.

Potential for Bitcoin in Underserved Communities

Bitcoin’s potential to revolutionize financial inclusion in underserved communities is undeniable. The very idea of circumventing traditional banking systems, with their often cumbersome regulations and high transaction fees, offers a compelling narrative. Imagine marginalized populations in remote areas gaining access to financial services previously unavailable. However, the realities of volatile markets, security concerns, and the need for widespread digital literacy must be acknowledged.

Traditional Banks’ Expanding Access, Bitcoin vs. Traditional Banking: What’s the Future?

Traditional banks are increasingly adopting innovative strategies to expand access to their services in underserved communities. These include mobile banking initiatives, partnerships with local financial institutions, and the development of innovative financial products designed to meet the specific needs of the target population. This drive is fueled by a combination of regulatory pressure, social responsibility, and the recognition of untapped market potential.

Comparative Analysis: Accessibility in Developing Countries

| Feature | Bitcoin | Traditional Banking |

|---|---|---|

| Internet Access | Requires internet connectivity, potentially limiting access in areas with poor infrastructure. | Often requires physical presence at a branch, although mobile banking options are emerging. |

| Financial Literacy | Requires understanding of cryptocurrencies and associated risks. | Often requires basic financial literacy, although varying levels of complexity exist. |

| Transaction Costs | Potentially lower than traditional banking fees in certain scenarios, but subject to high volatility. | Transaction costs can vary widely, depending on the type of transaction and geographical location. |

| Regulation and Security | Regulation is often nascent and varies across jurisdictions, posing potential security risks. | Governed by established regulations, offering some level of security but potentially facing compliance burdens. |

The table above provides a stark comparison, highlighting the unique challenges and opportunities presented by each system. The future, as always, remains uncertain, but the dynamic interplay between these two forces will undoubtedly shape the financial landscape for generations to come.

Investment and Speculation

The allure of Bitcoin, a digital gold rush, captivates investors with promises of astronomical returns. Yet, this siren song masks a volatile reality. Traditional banking, while offering a more measured approach, also presents opportunities for growth and security, albeit with different degrees of risk. This section delves into the stark contrasts in investment opportunities and the potential pitfalls of each system.The allure of Bitcoin lies in its potential for explosive growth, a tempting prospect for the speculative investor.

However, this potential is inextricably linked to its volatile nature. Traditional banking, while offering more predictable returns, is subject to market fluctuations, but in a far more controlled and less drastic fashion.

Bitcoin Investment Opportunities and Risks

Bitcoin’s decentralized nature opens doors to unique investment opportunities. Speculation fuels the market, driving prices to unprecedented highs and lows. Investors can buy and sell Bitcoin, hoping to profit from price fluctuations. The potential rewards are immense, but so too are the risks. The unpredictable nature of Bitcoin markets can lead to substantial losses.

The lack of regulatory oversight adds another layer of complexity and risk.

Traditional Banking Investment Options and Potential Returns

Traditional banking offers a range of investment options, from savings accounts to complex financial instruments. These options cater to various risk tolerances, from the safety of fixed-term deposits to the potential higher returns of stocks and bonds. The returns are typically more moderate than Bitcoin, but they are also more predictable and less volatile. The stability of traditional banking institutions provides a level of security often absent in the crypto market.

Speculative Nature of Bitcoin vs. Traditional Banking

Bitcoin’s inherent volatility and lack of established regulatory frameworks make it a highly speculative investment. Prices can fluctuate dramatically based on market sentiment and news cycles. Traditional banking, with its established regulatory framework and diversified investment options, offers a more stable investment environment. While not immune to market forces, the impact is generally more controlled.

Investment Strategies for Bitcoin and Traditional Banking

Bitcoin investment strategies often rely on technical analysis, market sentiment, and predictions of future price movements. Traditional banking strategies focus on long-term investment plans, risk diversification, and portfolio management, taking advantage of established financial tools. Bitcoin investors must be prepared for substantial price swings, while traditional banking investors can utilize tools like diversification and asset allocation to manage risk.

Role of Speculation and Volatility in Both Bitcoin and Traditional Banking

Speculation plays a significant role in both Bitcoin and traditional banking markets. In Bitcoin, speculation drives price fluctuations, leading to both immense gains and substantial losses. Traditional banking, while also influenced by market forces, operates with a more regulated framework, and therefore, less dramatic volatility. Both markets require a keen understanding of risk management to navigate their inherent volatility effectively.

Exploring the future of Bitcoin versus traditional banking systems is crucial. A key aspect of this involves understanding how legal recourse, like that offered by an insurance lawyer who makes companies pay what they owe, Insurance Lawyer Who Makes Companies Pay What They Owe , might influence the development of new financial frameworks. This legal expertise is relevant as digital currencies evolve, potentially impacting traditional banking models.

Ultimately, understanding these intertwined factors is essential for navigating the future of financial systems.

Future of Both Systems

The digital revolution is reshaping finance, and Bitcoin, the revolutionary cryptocurrency, stands poised to challenge the age-old edifice of traditional banking. This clash of titans will forge a new financial landscape, one where the very nature of value and trust is being re-examined. The future is not predetermined; it is a battleground where innovation and adaptation will determine the victor.

Bitcoin’s Technological Trajectory

Bitcoin’s future hinges on its ability to adapt and overcome inherent limitations. Increased scalability, enhanced transaction speeds, and improved energy efficiency are crucial for mainstream adoption. The emergence of layer-2 solutions and the development of more user-friendly interfaces are crucial steps towards making Bitcoin a viable everyday payment method. The evolution of decentralized finance (DeFi) protocols will play a significant role in Bitcoin’s future, potentially offering innovative financial services that bypass traditional intermediaries.

Furthermore, continued development in areas like privacy and security is paramount to fostering trust and encouraging broader use.

Examining Bitcoin’s future against traditional banking systems reveals complex questions. A key aspect involves understanding the intricacies of financial regulations, and a deep dive into this area is aided by insights from a powerful insurance lawyer who understands the industry’s hidden pitfalls, like Powerful Insurance Lawyer Who Knows the Industry’s Tricks. Ultimately, the future of Bitcoin and banking hinges on how these intricate legal and regulatory landscapes evolve.

This exploration is vital for making informed decisions about investments in this dynamic financial space.

Traditional Banking’s Adaptive Response

Traditional banking institutions are not passive observers in this digital transformation. Embracing technological advancements, such as blockchain technology and AI-powered risk assessment, is paramount. A crucial aspect of their future involves the development of more user-friendly digital platforms and personalized financial services. The integration of digital wallets, mobile banking, and secure online payment systems will be essential for staying competitive in a rapidly evolving landscape.

Furthermore, strengthening cybersecurity measures to counter cyber threats and ensuring compliance with evolving regulations are critical.

Integration and Coexistence

The future may not be one of outright replacement but rather one of integration and coexistence. Imagine a world where Bitcoin serves as a supplementary payment system for specific transactions, particularly cross-border transfers, while traditional banking continues to handle the majority of everyday transactions. The potential for cross-platform payments and streamlined integration with existing banking infrastructure will be crucial for the smooth functioning of this future financial system.

The development of hybrid solutions that combine the strengths of both systems could unlock unprecedented possibilities for financial inclusion and efficiency.

Evolution in Response to Emerging Technologies and Societal Shifts

The rise of decentralized autonomous organizations (DAOs) and the integration of NFTs into financial systems are reshaping the financial landscape. The future will see a confluence of technologies, with Bitcoin potentially integrating with these innovations. Traditional banks will need to adapt to these developments by offering services that leverage these technologies to enhance user experience and meet the evolving needs of customers.

The increasing importance of environmental consciousness and sustainability will likely influence both Bitcoin’s mining practices and traditional banking’s operations.

Potential Future Scenarios

| Scenario | Bitcoin’s Future | Traditional Banking’s Future |

|---|---|---|

| Scenario 1: Bitcoin Triumphs | Bitcoin becomes the dominant global payment system, replacing traditional methods for many transactions. | Traditional banks adapt by integrating Bitcoin and other cryptocurrencies into their services, or they decline into irrelevance. |

| Scenario 2: Coexistence and Convergence | Bitcoin coexists with traditional banking systems, used for specific purposes like cross-border payments or high-value transactions. | Traditional banks incorporate blockchain technology and cryptocurrencies into their operations, enhancing security and efficiency. |

| Scenario 3: Regulated Crypto Adoption | Bitcoin and other cryptocurrencies are regulated and integrated into the financial system, becoming a recognized asset class. | Traditional banks become more adaptable and flexible, incorporating new technologies to remain competitive. |

Emerging Technologies and Trends

The digital landscape is in constant flux, with revolutionary technologies poised to reshape the very fabric of finance. This relentless innovation is not merely a trend; it’s a seismic shift, threatening to obliterate the established order and usher in a new era of financial possibility. The clash between Bitcoin’s decentralized ethos and the traditional banking system’s entrenched infrastructure is set to be dramatically influenced by these emerging forces.The relentless march of technological advancement is rewriting the rules of engagement in the financial realm.

From decentralized finance (DeFi) protocols to quantum computing, the potential for disruption is both exhilarating and terrifying. These technologies are not simply adding features; they are fundamentally altering the underlying principles of both Bitcoin and traditional banking, creating new vulnerabilities and unprecedented opportunities.

Impact of Blockchain Technology on Traditional Banking

Traditional banking, historically resistant to change, is now grappling with the transformative potential of blockchain technology. Blockchain’s inherent immutability and transparency offer a compelling alternative to traditional record-keeping methods. This could revolutionize the way banks manage transactions, reducing fraud and increasing efficiency. The potential for faster, cheaper cross-border payments is also significant. However, implementing blockchain across the vast and complex network of traditional banking is a monumental task.

Interoperability between different blockchain platforms and the integration of existing legacy systems are significant hurdles. Challenges remain in regulatory frameworks and public acceptance, but the potential is undeniable.

Influence of New Technologies on Bitcoin

Bitcoin, a digital gold standard built on the bedrock of cryptography, is not immune to the disruptive power of emerging technologies. The burgeoning field of decentralized finance (DeFi) is proving to be a fertile ground for innovation, with decentralized exchanges and lending platforms emerging as viable alternatives to traditional financial institutions. The integration of Artificial Intelligence (AI) could enhance transaction security and improve user experience, potentially streamlining Bitcoin’s already decentralized architecture.

However, the inherent volatility of Bitcoin’s price and the security of the underlying blockchain remain critical considerations.

Examples of Emerging Technologies Impacting Both Systems

- Decentralized Finance (DeFi): DeFi platforms are rapidly changing how financial services are delivered. This technology enables peer-to-peer lending, borrowing, and trading without the need for intermediaries. This has a potential disruptive impact on both Bitcoin and traditional banking, potentially undermining traditional financial institutions while also creating new opportunities for innovation and accessibility.

- Artificial Intelligence (AI): AI can be utilized to improve fraud detection and enhance security measures in both Bitcoin and traditional banking systems. Its ability to process vast amounts of data can lead to more accurate risk assessments and personalized financial services.

- Quantum Computing: Quantum computing, though still in its nascent stages, could potentially break current encryption methods, posing a significant security risk to both Bitcoin and traditional banking systems. However, it also has the potential to unlock new cryptographic solutions to enhance security in the future.

- Central Bank Digital Currencies (CBDCs): Central banks worldwide are exploring the creation of digital currencies. This could potentially disrupt Bitcoin’s position as a leading digital asset. However, the specific implementation and regulatory framework of each CBDC will determine its impact.

Disruptive Technologies for Both Systems

Several emerging technologies hold the potential to fundamentally disrupt both Bitcoin and traditional banking systems. Their disruptive nature stems from the potential to alter core functionalities and business models. These technologies include:

- Decentralized Finance (DeFi): This system is poised to challenge the traditional financial infrastructure, offering a more transparent and accessible alternative to traditional banking services.

- Artificial Intelligence (AI): AI can significantly influence both systems, enhancing security and automating processes. This can lead to a faster and more efficient financial landscape, but also create new vulnerabilities.

- Blockchain Technology: Blockchain’s inherent transparency and security could reshape traditional banking processes, while Bitcoin’s reliance on blockchain is at the core of its value proposition.

Expert Opinions

“The future of finance is decentralized. While traditional banking institutions will undoubtedly adapt, the decentralized nature of Bitcoin and blockchain technology will increasingly shape the financial landscape.”Dr. Anya Sharma, Fintech Expert

Bitcoin as a Payment System

Bitcoin, a revolutionary digital currency, presents a disruptive force in the realm of global payments. Its decentralized nature and purported immutability promise a paradigm shift, challenging the established order of traditional banking systems. However, the path to mainstream adoption is fraught with obstacles, demanding a careful assessment of its strengths and weaknesses.Bitcoin, despite its promise, faces significant hurdles in becoming a universally accepted payment method.

The volatility of its price, coupled with regulatory uncertainties, creates considerable risk for merchants and consumers. The intricacies of its technical architecture, while lauded by some, can be daunting for the average user. This complexity contributes to the challenges of widespread adoption.

Bitcoin’s Viability as a Payment Alternative

Bitcoin’s potential as an alternative payment system hinges on its ability to overcome the limitations of traditional systems. Its decentralized nature, purportedly immune to central control, attracts those seeking an alternative to established financial institutions. Bitcoin transactions, while theoretically instantaneous, often suffer delays and high transaction fees in practice. Moreover, the lack of consumer protections and the potential for fraud are serious concerns.

Comparison to Traditional Payment Systems

Bitcoin’s capabilities are best assessed in comparison to existing payment methods. Credit cards, with their established infrastructure and global acceptance, offer a streamlined user experience. Bank transfers, while secure, often suffer from processing delays and varying fees based on transaction specifics. Bitcoin, while offering some potential advantages in terms of decentralization, falls short in terms of widespread user adoption and practical applicability.

Advantages of Bitcoin Payments

Bitcoin’s advantages include its potential for lower transaction fees compared to traditional systems, especially for cross-border payments. Its decentralized nature theoretically eliminates intermediaries, reducing costs and potentially increasing transparency. However, these potential benefits are often tempered by the practical realities of high transaction fees, volatility, and security concerns.

Disadvantages of Bitcoin Payments

Bitcoin’s disadvantages include its inherent volatility, making it a risky payment option. The lack of consumer protections and the potential for fraud pose significant challenges. Its technical complexity, while a feature for some, serves as a barrier for the average user and merchant.

Comparison Table

| Feature | Bitcoin | Credit Card | Bank Transfer |

|---|---|---|---|

| Fees | Variable, potentially low but often high | Low to moderate, often dependent on transaction type | Low to moderate, often dependent on transaction type |

| Speed | Variable, often faster than bank transfers, but can be slow | Instantaneous | Variable, often slower than credit cards |

| Security | High, but vulnerabilities exist | High, but fraud is possible | High, but fraud is possible |

Final Wrap-Up

So, Bitcoin vs. Traditional Banking: What’s the future? The answer’s not so clear-cut, fam. Both systems got their pros and cons, and the future likely involves some kind of integration. Bitcoin offers a different approach, but traditional banking’s got the established infrastructure and trust.

Ultimately, it’s all about finding the right balance, the best way to use both for a solid financial future, and figuring out how to handle the inevitable shifts and surprises.

Question & Answer Hub

Is Bitcoin more secure than traditional banking?

No single answer, my dude. Bitcoin’s decentralized nature makes it potentially harder to hack, but traditional banking has sophisticated security systems. It depends on the specific methods and how well they’re protected.

Can Bitcoin replace traditional banking completely?

Nah, not likely. Traditional banking offers a lot of services and trust that Bitcoin’s still building. They probably will co-exist, or integrate in some way.

What are the biggest risks of investing in Bitcoin?

High volatility, man. Bitcoin’s value can fluctuate wildly. Also, regulation is still developing, so there’s uncertainty about the future of the crypto world.

How accessible is Bitcoin in developing countries?

It’s more accessible than traditional banking in some areas, but it depends on the specific region and infrastructure. Bitcoin’s potential to improve financial inclusion is real, but it also faces obstacles like internet access and understanding.